Dreaming of taking your expertise to the global stage?

The Institute of Chartered Accountants of India (ICAI) is opening doors for Indian CAs to claim their rightful place in the International Accounting market through its latest initiative and to cater to the increasing overseas demand for CAs. But what exactly is this initiative, and how…

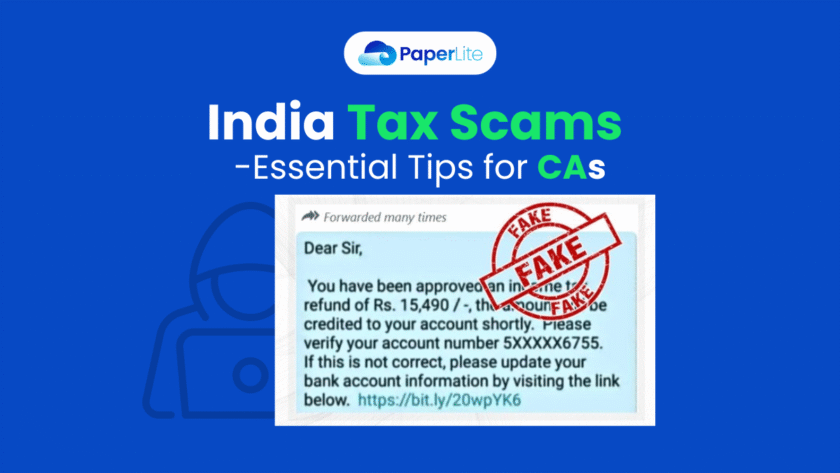

Tax season in India ushers in a busy period for Chartered Accountants and Accounting Firms. However, alongside the rush of filings and consultations comes an unfortunate reality – a drastic rise in tax-related scams targeting unsuspecting individuals and businesses across India.

In recent times, there has been quite a surge in tax-related scams, particularly those…